What is RTP® Surcharging? How Does It Work?

Eliminating Merchant Processing Fees with Payer-Covered Costs

RTP® Surcharging – Payer-Covered Merchant Processing Fees for Real-Time Payments

A New Era of Business Payments with RTP® Surcharge

Merchants today are burdened with high processing fees and slow payment settlements, whether they rely on credit cards, ACH transfers, or wire payments. Traditional payment processing challenges include:

- Credit card interchange fees cutting into profit margins

- ACH transaction delays that slow down business cash flow

- Hidden merchant fees that reduce overall revenue

By adopting the RTP® Surcharging method, businesses can:

✅ Pass processing fees to the

payer (customer/client) for real-time transactions

✅

Enable instant A2A Credit & Debit transactions via RTP® and Same-Day

ACH

✅ Use POS, MOTO (Mail Order/Telephone Order),

Auto-Bill Pay, and invoicing

✅ Ensure compliance

with Federal & State regulations for payment processing

✅

Leverage ISO 20022 messaging for secure, automated, and structured

payments

With TodayPayments, businesses can accept RTP® payments instantly—without incurring merchant processing fees.

RTP® Surcharging vs. Traditional Payment Processing

RTP® Surcharging is a payment model where the payer (customer) covers the merchant’s transaction fees, reducing costs for businesses.

✔ The Payee

(merchant/business) applies an RTP® surcharge – typically a

small percentage of the transaction.

✔ The

Payer (customer/client) covers the processing fee at checkout.

✔ Funds settle instantly, ensuring immediate

access to cash flow.

✔ Applies across

multiple payment channels: POS, MOTO, Auto-Bill Pay, and

invoicing.

Why Businesses Are Adopting the RTP®

Surcharge Model:

✔ Minimizes

operational costs by shifting fees to the payer

✔

Encourages fast, secure, real-time transactions over credit cards

✔ Provides full transparency while complying with

State & Federal regulations

RTP® Surcharging vs. Traditional Payment Processing

Why Businesses Should Transition to RTP®

|

Feature |

RTP® Surcharge Model |

Traditional Merchant Fees |

|

Processing Speed |

Instant (24/7/365) RTP® & Same-Day ACH payments |

ACH: 1-3 days, Credit Cards: 1-5 days |

|

Merchant Processing Fees |

Paid by Payer (Customer/Client) |

Absorbed by Merchant |

|

Bank Reconciliation |

Automated via ISO 20022 Messaging |

Manual reconciliation required |

|

Chargeback & Fraud Risk |

Low (RTP® payments are final and irrevocable) |

Higher risk with credit card chargebacks |

|

Customer Payment Experience |

Transparent pricing with a disclosed surcharge |

Hidden processing costs for merchants |

Why Businesses Are Switching to RTP®

Surcharging:

✔ Eliminates costly

merchant processing fees

✔ Ensures immediate

payment settlements and improves cash flow

✔

Reduces chargeback risks compared to credit card transactions

How RTP® Surcharge Works for POS, MOTO, Auto-Bill Pay & Invoicing

Seamless Integration for Multiple Payment Channels

With TodayPayments' RTP® integration, businesses can apply surcharges across various payment environments:

Point of Sale (POS):

Implement RTP® surcharges at checkout for in-person transactions.

Mail Order / Telephone Order (MOTO): Apply

surcharges for phone-based transactions.

Auto-Bill Pay: Automate recurring payments while passing fees

to the payer.

Invoicing & Online Payments:

Include an .html payment link with a disclosed surcharge

for customers.

How It Works:

✔

Step 1: Business applies an RTP® surcharge on

transactions

✔ Step 2: The customer

selects RTP® as the payment method and sees the surcharge

✔ Step 3: The total transaction amount

(including surcharge) is processed instantly

✔

Step 4: Funds are settled immediately, and businesses

receive full payment without deductions

This model eliminates hidden processing costs for businesses while giving customers a transparent, real-time payment option.

Federal & State Regulations on RTP® Surcharging

Ensuring Compliance Across All U.S. Jurisdictions

RTP® transactions are governed by Federal Reserve regulations, which allow merchant surcharging in accordance with applicable state laws.

- Credit Card Surcharges Are Regulated by State Law: Some states prohibit credit card surcharges, but RTP® payments are direct A2A transactions and do not fall under credit card surcharge regulations.

- Cash Discount Programs Are Legal in All 50 States: RTP® payments may qualify as an alternative cash discount program, ensuring compliance in all jurisdictions.

- Federal Compliance: As a federally backed system, RTP® enables compliant payment processing with transparency and fee disclosure requirements.

Best Practices for RTP® Surcharge

Implementation:

✔ Clearly disclose

surcharges before payment processing

✔ Ensure

compliance with both state and federal payment regulations

✔ Leverage ISO 20022 messaging for transparent and

structured payment requests

ASK us how:

"How to implement RTP® Surcharge for

instant A2A transactions"

"Best surcharge model for RTP®

payments in POS, MOTO, Auto-Bill Pay, and Invoicing"

"ISO 20022 messaging for compliant, real-time payment

reconciliation"

"How businesses can pass payment

processing fees to customers using RTP®"

"Federal and

State regulations on surcharging for RTP® real-time payments"

Surcharging and Cash Discounts

with FedNow®:

The payment processing

method application of surcharging or cash discounts to FedNow®

transactions is not explicitly addressed in current Federal or

state laws, which primarily focus on credit card transactions.

However, the principles may be analogous:

• Surcharging:

Applying a surcharge to FedNow® payments could be subject to

similar regulations as credit card surcharges, depending on state

laws. Merchants should exercise caution and consult legal counsel

before implementing such fees.

• Cash Discounts:

Offering discounts for using FedNow® payments is generally

permissible nationwide, aligning with the legal status of cash

discount programs.

Upgrade to RTP® Surcharge Payments with TodayPayments

For businesses looking to eliminate payment processing fees, improve cash flow, and accelerate transactions, the RTP® Surcharge model is the perfect solution.

With

TodayPayments, businesses can:

✔

Enable payer-covered processing fees for instant payments

✔ Accept payments across POS, MOTO, Auto-Bill Pay,

and invoicing

✔ Provide a real-time, low-cost

alternative to credit card transactions

✔ Automate

reconciliation and eliminate chargeback risks

✔

Ensure full compliance with Federal and State regulations

Upgrade your payment processing—implement the RTP® Surcharge model today!

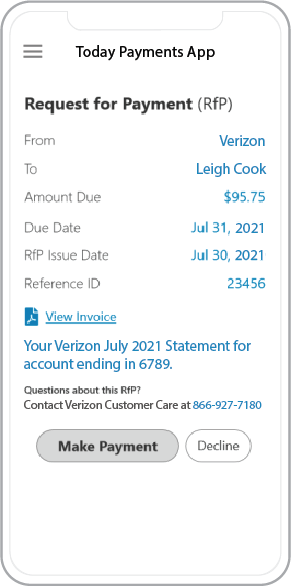

Creation Request for Payment Bank File

Enhance Your FedNow Surcharging using Real-Time Payments Requests with FedNow’s ISO 20022 Messaging

Streamline Payments with Advanced Request for Payment Options:

Harness the power of FedNow's Request for Payment system to transform how you manage invoices and remittances. Our platform supports diverse data integration options, allowing payees to incorporate detailed invoice data directly within the RfP message or link to a comprehensive Merchant Page.

Flexible Invoice Details with ISO 20022 Messaging:

Leverage the flexibility of ISO 20022 messaging standards in our RfP system. You can choose to display crucial payment details directly in the message with a concise 140-character description, or through a dynamic "Hyper-Link" leading to a detailed Merchant Page. This Merchant Page can be hosted either on your website or TodayPayments.com/HostedPaymentPage.html through our seamless integration solution.

Customizable Merchant Pages for Enhanced Customer Experience:

Create a Merchant Page that not only details all the MIDs you own but also presents these options attractively to your customers through the RfP. This customization ensures that whether your payer opts for Real-Time Payment, Same-Day ACH, or Card transactions, they can easily navigate and complete their payments through a simple click on the hyperlink provided on your Merchant Page.

Call us today and receive the .csv or .xml FedNow® or Request for Payment (RfP) file you need—all during your very first phone call! We guarantee that our comprehensive reports integrate flawlessly with your bank or credit union. As pioneers in recognizing the benefits of RequestForPayment.com, we have stayed years ahead of our competitors. Although we are not a bank, our role as an "Accounting System" within the Open Banking ecosystem enables us to work with billers to create effective RfP files that seamlessly upload to the biller's online banking platform. U.S. companies rely on our expertise to learn how to deliver the RfP message directly to their bank with precision.

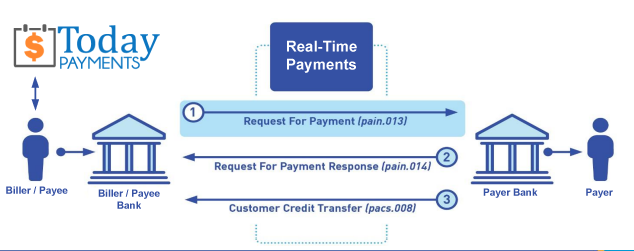

Our advanced solution, Today Payments' ISO 20022 Payment Initiation (PAIN.013), demonstrates how to create a Real-Time Payments Request for Payment file that sends a clear message from the creditor (payee) to its bank. Most financial institutions support the import of messaging and batch files for both FedNow® and Real-Time Payments (RtP), ensuring smooth processing. Once the file is correctly uploaded, the creditor’s bank processes the payment through a secure "Payment Hub"—with The Clearing House serving as the RtP Hub—and relays the message to the debtor's (payer's) bank. This streamlined approach not only accelerates transaction processing but also enhances transparency and reliability for all parties involved.

... easily create Real-Time Payments RfP files. No risk. Test with your bank and delete "test" files before APPROVAL on your Bank's Online Payments Platform.

Today Payments is a leader in the evolution of immediate payments. We were years ahead of competitors recognizing the benefits of Same-Day ACH

and Real-Time Payments funding. Our business clients receive faster

availability of funds on deposited items and instant notification of

items presented for deposit all based on real-time activity.

Dedicated to providing superior customer service and

industry-leading technology.

Contact Us for Request For Payment payment processing